Find out if your current retirement savings are on track

As retirement nears—especially as your number of remaining working years drops into the single digits—it's time to evaluate your retirement readiness.

Up to now, retirement planning may have been vague, with only broad ideas about what you might do and what things might cost. You've been saving for retirement most of your life, but you don't really know if it's enough.

As you approach retirement age, it's crucial to go through a retirement checklist to determine where you stand.

Here are four steps to help you get organized and prepared for retirement.

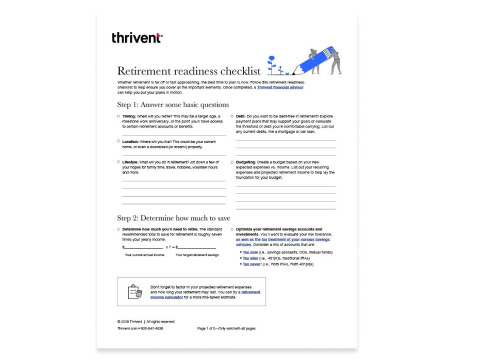

Step 1: Start by answering some basic retirement planning questions

Having a vision of your post-work life gives you a goal that can drive your financial decisions. It can shape how long you need to save, how much you need to save and how you'll spend what you've saved. Start by answering these

☐ When will you retire?

Some people have an age, a number of working years or a milestone they're aiming to reach before starting retirement. There aren't any retirement rules that say when you have to stop working. However, age does dictate when you:

- Have access to your tax-advantaged retirement accounts, like a 401(k) or traditional IRA without penalty (at least age 59½).

- Can

claim Social Security retirement benefits. (Claimingas early as age 62 means a reduced amount while holding off until age 70 means a maximum amount.) - Have to take

required minimum distributions (RMDs) from tax-deferred retirement accounts, such as 401(k)s or 403(b)s (age 73 for those born before 1960, and age 75 for those born in 1960 or later).

When to retire is entirely up to you. You may consider:

- What feels like the right age to stop working?

- Do any retirement benefits depend on a number of years of service at your job?

- Is early retirement your plan, or do you want to delay as long as possible?

- How does your health and life expectancy factor in?

- Does your family situation affect when you start retirement?

Even if you don't know for sure, an approximation can give you a working timeline so you can set milestones. Make sure to discuss these questions with your partner, too.

☐ Where will you live when you retire?

Retirement can be a chance to settle down or change things up. Personal and financial reasons will influence your options, but it's important to narrow it down so you can plan for what you want. Think through the possibilities:

- Keeping your home. Particularly if you've already paid off your mortgage, you may want to stay where you are for as long as possible. You also could consider turning your home into a rental property for retirement income.

- Downsizing your home.

Relocating to a smaller or less expensive home could save you time, effort and money in your retirement years. Especially if your plan is to age in place, your home should be a manageable size for upkeep and repairs.

- Moving for a lower cost of living. In retirement, your priorities shift. Living close to your work or residing in a certain school district may not be important now. Lower taxes, affordable housing and public transportation could draw you elsewhere and make your retirement dollars last longer.

- Moving where you want, even if it costs more. You want a retirement that you'll enjoy, so don't neglect the nonfinancial reasons for a retirement location. Living near family, having certain amenities, being near the water or the mountains—many things can influence your retirement dream.

☐ What will you do when you retire?

When you're not working a full-time job, you have plenty of time for other things. Think about how you want to spend your days so you'll know what expenses or income may be involved:

- How will you remain active and engaged?

- What passions and hobbies do you want to pursue?

- Are there clubs, church groups or special-interest organizations you'd like to join?

- Will you want to keep working or start a business?

- Do you have plans to volunteer or take on a nonprofit project?

☐ What debt will you carry into retirement?

Eliminating debt before retirement is a common goal for many aspirational retirees. And while it certainly has its benefits, it may not be necessary based on your financial resources and personal goals.

Ask yourself:

1. Can you afford to have debt?

A common question is whether or not to pay off your mortgage before retiring or if you should keep other

2. Do you want to carry debt into retirement?

Even if you can afford to carry some debt, you may not want to. Debt can strain your budget and cause you stress. If paying off all your loans and bills before you stop working will make you feel more relaxed, then it's a smart use of your money and may mean you enjoy your retirement more.

It's also essential to have a plan to avoid accumulating debt in retirement.

- If you expect your debt to grow in retirement, you may not have a sound budget.

- Unexpected expenses can happen at any time, so

build an emergency fund to help avoid further debt and protect your financial picture.

Get more guidance on debt management in retirement

☐ What will your retirement budget be?

Creating a retirement

Review the income and expenses you have now and consider the following:

- What work-related costs (i.e., lunch, commuting, clothing) will go down? What discretionary spending (think travel, entertainment and leisure) may go up?

- If you're planning to move—regardless of whether you're downsizing locally or relocating to a new city, state or country—how will that affect your expenses?

- What else might change from your current budget? Will your income be more or less? Will your expenses, spending and charitable giving be more or less?

Step 2: Determine how much to save for retirement

Once you know your retirement budget, you can better plan for how you'll support it. Lining up the details of what you want your retirement to look like with what you've accumulated in your savings—or expect to—is essential for gauging your retirement readiness. At the end of this step, you'll know if you have realistic expectations or if you need to go back and adjust some of the parts in Step 1.

☐ How much money do you need to retire?

Everyone's answer is different, but a general guideline is building up retirement savings that's about seven to eight times your annual income. Since you've already worked up a budget in Step 1, you're already on the way to finding an answer that's more personal to you:

- Estimate. Gauge if you have enough money to retire by taking your projected retirement expenses, anticipating how long your retirement will last and comparing it to what your projected savings and retirement income will be.

- Calculate. With workable numbers for your planned sources of income, annual savings rates and your spending in retirement, you can find out how long your money might last. Using a

retirement income calculator makes it easy.

- Double up. If you're married, consider how much money a

couple needs to retire. Consider the expenses you share as well as the savings opportunities you have and how you can take advantage of them. For example, if you both work and have workplace retirement plans, you can each save to the maximum individual limit but plan to spend it together.

Find out if your current retirement savings are on track

☐ How to maximize your retirement savings

Based on those projections, if you find you don't have enough savings to meet your retirement goals comfortably, it's crucial you use the time you have to get back on track. Consider all the tax-advantaged retirement savings opportunities available to you:

- Get the most out of your 401(k). Make sure you're taking full advantage of employer

matching contributions . If you're already saving enough to receive the full match, considermaxing out your 401(k) or other employer plan. These accounts have much higherannual contribution limits than IRAs.

- Look for ways to catch up. Once you reach age 50, retirement accounts like 401(k)s, 403(b)s and IRAs allow you to put in extra money.

Catch-up contributions on top of contributing the usual maximum limits let you reduce savings gaps.

- Go beyond your employer's plan. You can

open an IRA on your own even if you contribute to a workplace retirement plan. Deductibletraditional IRAs let you defer taxes until you withdraw money later whileRoth IRAs are funded with after-tax contributions but allow the opportunity for tax-free withdrawals in retirement. (With an IRA and a Roth, verify that you don'texceed the income limit before contributing to one.)

Ways to continue to build retirement savings

If you do reach the annual limits on your employer plan and IRA contributions, you still have options for building savings to use in retirement.

You could:

☐ How are you investing for retirement?

Contributing to a tax-advantaged retirement account is only one piece of the saving process. You'll also need to decide how to

- Aggressive approach. When you're working and saving for a retirement date that's still many years away, investing for growth might be your primary goal. A portfolio tilted toward more aggressive equity investments may be a good fit.

- Moderate approach. As you get closer to retirement, you may want your investment focus to shift away from growth and toward stability to support your withdrawals.

- Finding balance. Your retirement is likely to last several decades. Be sure to maintain a balance of investments that will allow your portfolio to outpace inflation and provide the return you need to ensure your money lasts while also allowing you to take withdrawals when you need them.

Step 3: Prepare your retirement income plan

After evaluating whether you've saved enough for a comfortable retirement, it's essential to make a plan for how you'll turn your savings and other sources of money into a regular stream of income that can support you for the long haul. Taking a structured approach can give you more confidence your

☐ Evaluate your retirement income sources

Your savings account doesn't have to be your only

Personal retirement accounts

It's possible to have multiple employer and individual retirement accounts. Make sure you've accounted for them all and that you know what you can do with them:

- Did you have another job with an employer-based retirement account that you let sit? Now's the time to think about

rolling it into an IRA for easy access. - Are you in your 50s but not yet 59½ and facing the possibility of quitting, getting laid off or retiring extra early? If so, the

rule of 55 may help you access your current employer retirement savings account penalty-free. - Consider all of the

options for your 401(k) when you retire . You may want to leave it in the plan, roll it into an IRA or take a distribution and invest it elsewhere if it's to your advantage.

When to claim Social Security

Social Security is a guaranteed,

- Age. Choose the age you want to

claim your Social Security benefit carefully. Taking it before yourfull retirement age means you permanently receive a lower monthly payout. Delaying (up to age 70) means you get a higher monthly payout for the rest of your life. - Marital status. If you're married, coordinate your

Social Security benefits with your spouse . You may want to both claim at the same time, or you may want the higher-earning spouse to wait longer to optimize benefits. This often is called a staggered or split strategy.

Pension income

Pension plans can provide a firm foundation for your retirement, but some factors surrounding

- Consider a lump sum if:

- You need the money now.

- You fear the pension plan could go bankrupt.

- You want to ensure you can pass it on to your heirs.

- Consider monthly payments if:

- The amount will adjust for inflation.

- Your spouse would continue to receive a benefit if you die.

- You think you will live a long time and don't want to run out of money.

Consider an annuity as a source of guaranteed income

An

Immediate annuities. Turn a lump sum of money into a fixed income stream, taking some of the uncertainty out of your distribution plan.Deferred annuities. Begin your payouts at a later date, which can allow you to spend from your other retirement savings without worrying as much about making it last, knowing that this additional income stream will be coming.

Cash value life insurance can supplement your retirement income

While the main point of life insurance is to provide for a loved one if you die, your

☐ Choose a retirement withdrawal strategy

The foundational retirement income you can count on includes Social Security, pension and annuity income, plus any life insurance cash value you intend to draw. Aside from setting these in motion, you won't have to do much calculating or maintenance to know what you're getting on a regular basis.

For the rest of your savings and investment accounts, it's crucial to calculate and plan your retirement withdrawals so you don't take out too much money too early and run out. Consider these key decisions when it comes to withdrawals:

Structuring your retirement withdrawals

A systematic withdrawal strategy helps you strike a balance between covering your living expenses throughout retirement and avoiding the

Among the approaches to take, a common starting point is

This rule may not be the best

Factoring in required minimum distributions (RMDs)

Pay attention to

You'll have to decide how to handle your RMDs:

- Factor them into your spending plan.

- If you don't immediately need this money, put it somewhere where it has the potential to grow, like a

certificate of deposit (CD) orbrokerage account. - Consider a

qualified charitable distribution (QCD) with unneeded IRA funds to help reduce your tax bill.

Step 4: Protect your retirement savings

Being fully retirement ready means you've also prepared for

☐ Estimate potential health care costs in retirement

It's no secret that the average cost of health care rises the older you get. Plan ahead so you can navigate these expenses without sacrificing your financial security.

Long-term care

Most seniors will have long-term care needs during their lifetime. It could be a matter of a few months while you recuperate or several years if you develop a condition. Have a plan to pay for it. Use a

Health insurance in retirement

If you're at least age 65, you can

☐ Factor in the effects of inflation in retirement

Prices usually increase over time due to inflation. Your expenses will go up, but that doesn't have to mean disaster if you account for it. Take steps to

- Add it in your budget. Use an

inflation estimate of 4% to adjust your budget going forward. You don't have to (and frankly, can't) know an exact future inflation rate for this. But it pays to factor for it in some capacity.

- Invest with inflation in mind. If you're too conservative with your investments, you could miss out on growth opportunities. Maintaining an allocation to stocks can help your portfolio keep pace with inflation but comes with a risk of loss. Consider

hedging against inflation by keeping a portion in inflation-protected investments, such asTIPS or I bonds, to provide a fixed real rate of return.

☐ Manage your taxes in retirement

Strategically navigating

Know how your retirement income sources will be taxed . Consider your current and future tax filing status. What you pay in taxes now may be different when you shift to your retirement income. It's crucial to watch your income—and if you're married, your combined income—so you can create a tax-smart plan around your lifetime savings.- Taxed upon withdrawal at ordinary tax rate: Traditional IRAs, traditional 401(k)s or other employer plans, pensions, annuities, HSA withdrawals for nonmedical expenses after age 65

- Taxed annually between 0%–20%: Qualified dividends and capital gains from nonretirement investment accounts

- Not taxed annually or upon withdrawal: Qualified Roth IRA and Roth 401(k) or other Roth employer plan withdrawals, HSA withdrawals for qualified medical expenses

Understand how Social Security is taxed. Depending on your income, up to 85% of your Social Security benefit may be subject to federal taxes.

Weigh if a Roth conversion makes sense. If you're in a lower tax bracket now than you will be once Social Security, pensions and RMDs kick in, you may consider converting from a traditional to a Roth IRA. While you may incur expenses upfront for this conversion, you'll allow your money to grow tax-free and be able to take tax-free withdrawals of earnings (after the account has been in place five years) for the rest of your life.

Be prepared for tax changes with a spouse's death. Tax brackets favor couples in terms of both rates and deductions. When a spouse dies, the surviving spouse may move to a higher tax bracket and have a lower standard deduction.

☐ Prepare your retirement savings for market volatility

If you run into

- Keep some cash in reserve.

Holding enough cash or fixed investments to get you through the first few years of expenses can shield you from the effects of a poor sequence of stock market returns. It's not for everyone, so consider if it's realistic for you and how much short-term savings you can afford to maintain.

- Be financially and emotionally ready. Your own emotions can be the biggest source of investment risk. Panicking and abandoning your investment plan when things get bumpy can cause losses.

☐ Factor longevity risk into your retirement plan

Living a long life is something a lot of people strive for. But if you live longer than you plan for, you may deplete your savings too soon. You need to safeguard against

- Account for longevity risk in your withdrawal plan. Don't underestimate your life expectancy and risk running out of money too early.

- Maximize your Social Security and pension income. This ensures you have a firm base of inflation-adjusted, guaranteed income that won't run out.

- Consider that annuities can provide lifetime income. Whether you use an immediate annuity with payouts that start right away or a deferred annuity that starts payments later, having annuities in your mix can provide protection from longevity risk. You even can purchase annuities inside tax-deferred retirement accounts.

Qualified longevity annuity contracts (QLACS) allow you to purchase income annuities without violating RMD rules.